The Glittering Gift of Gold

- Laura Malone

- Dec 15, 2025

- 2 min read

When we think of donating to charity, we often look at our checkbook as the primary source of giving. We perhaps never think of gold or other precious metals like silver or platinum, for the simplest reason of accessibility. The average person does not have their wealth in bullion. It is estimated that as little as 10% of the US population have any holdings in gold, and other precious metals are even less.

Those who have holdings in precious metals usually have made that financial decision as a hedge against inflation. When a currency becomes devalued, a precious metal can be a source of stable value or even growth during inflationary times. It is a finite, tangible asset; in the case of gold, it has been a store of value that has been relied on by civilizations for nearly 3000 years.

For those who hold precious metals, regarding that tangible value as a tool for charitable giving deserves consideration. We’ll look into the tax implications of this process and some of the hurdles of being able to turn bullion into charitable good.

Tax Implications of Donating a Precious Metal

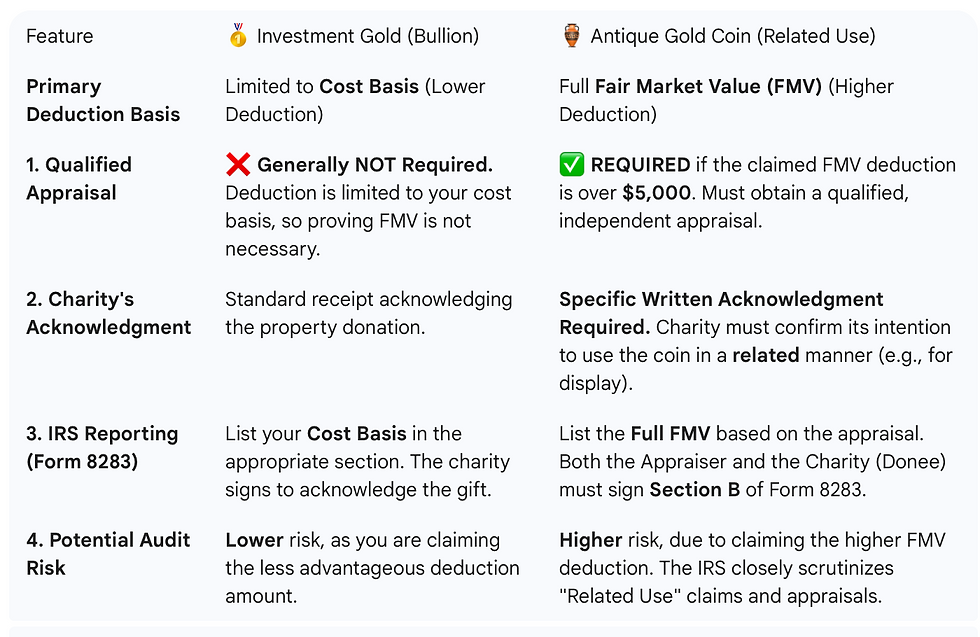

When donating appreciated assets like physical gold, the donation is subject to the crucial "Related Use" rule because the IRS classifies all physical precious metals ( such as gold bars, gold rounds, or government-issued bullion coins like American Eagles ) and historic coins as "collectibles." This rule dictates the amount you can claim as a tax deduction.

If the charity uses the donated asset for a purpose related to its tax-exempt function (e.g., a museum displaying a rare gold coin that was donated to it), you can deduct the asset's full Fair Market Value (FMV). However, if the use is deemed unrelated (which is the most common scenario for investment bullion, as most charities immediately sell the gold for cash) your charitable deduction is limited to your original cost basis (what you paid for the gold). A direct donation does however allow you to successfully avoid paying capital gains tax on the appreciation.

The Mechanics of Giving Gold

For ease of illustration, we will focus on gold as our precious metal for discussion. One of the first considerations that a donor must consider is if their selected charity can accept a gift of gold. Some organizations may not have the financial experience or capacity to be able to accept such a gift.

Another concern is if the gift can be used as a Related Use for the selected charity ( such as a historic gold coin put on display at a museum), or if the gift is investment gold intended to be liquidated for cash.

Documenting the process and what is required is below:

Conclusion

For many donors and charities, precious metals such as gold are likely to be considered as unorthodox. The process is complicated, with a variety of documentation needs and steps required. However, for those donors with such holdings and those charities willing to accept them, the gift can of charitable value to both.

At Generosity Nexus, we have the ability to provide guidance and draw on the expertise of other experts in addressing the tax concerns and giving implications that precious metals represent.

Don’t hesitate to schedule an appointment to learn more about how we can help you.